Having insurance for your fine art and decorative art is an important part of owning a collection.

The power of the fine and decorative art market

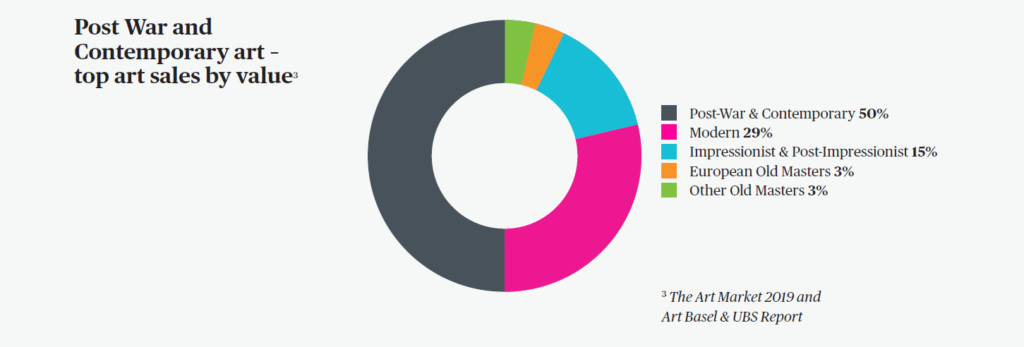

Over the past decade the art market has become truly global, although the United States, China, and the UK still account for the vast majority of sales. As new audiences gain exposure and access to artwork and collectibles of all kinds, sales have trended upwards, with an overall increase in sale totals of over 60%.(1) Online sales also continue to increase, with a growing number of collectors turning to digital platforms to acquire artwork. Online sales are particularly strong among millennial collectors.(1)

Female artists are attracting attention(2)

While men have overshadowed their female counterparts in the art world for centuries, many women artists are now getting due recognition for their contributions to influential art movements, with major museum retrospectives, gallery shows and rising values. Two top female artists include Yayoi Kusama (born in 1929) and Joan Mitchell (1925-1992). Kusama, a renowned provocative avant-garde artist from Japan, brought in the highest sales at auction in 2018, with a total of $86.4 million. Mitchell, a leading abstract expressionist American painter, was a close second, with sales totaling $83.5 million at auction, and an individual record set of $16,625,000, including buyer’s premium, for her 1969 painting “Blueberry”.

Not all art enthusiasts fully insure their collection

While some art enthusiasts take pride in making sure their collections are protected in case of damage or loss, a surprising number are still uninsured or underinsured, especially if their collections haven’t had an appraisal on a regular basis.

5 reasons to look for the art insurer

It’s important to fully insure your artwork. If you don’t believe you need insurance to protect your fine and decorative art, here are a few reasons to reconsider:

1. Your homeowner’s policy may not cover your art.

A typical homeowner’s policy is designed primarily to protect your home, personal liability, and the general contents of your home. Relying solely on your homeowner’s policy may mean paying significant out-of-pocket expenses if your artwork is lost, stolen or damaged. Fine art insurance policies provide “all-risk” coverage for most causes of loss, with no deductible. Some insurance companies cover fine and decorative art items valued at less than $250,000 without an appraisal. The insurer just needs a good description of the item as well as the estimated value.

2. The right policy can provide more than cash for a loss.

Caring for your art collection can be complicated. If you’re not sure how to best do this, you’ll want experts on hand to help. You will want an insurance company that provides a full suite of consultative collection management services to complement their policy. An insurance company with highly trained in-house Fine Art & Collections Specialists can provide:

- A collection risk assessment at your home, office, or off-site location

- Guidance on proper storage and display conditions

- Fire protection and security recommendations

- General advice about preserving your collection

- Referrals to art professionals

3. If your art is lost or stolen, you’ll want to replace it.

Look for a fine and decorative art policy that will cover misplaced, lost, or stolen items. And, if the market value of an itemized article exceeds the amount listed in the policy right before it is lost or stolen, you’ll want an insurance company that will pay the higher market value, up to 150% of the itemized amount, so that you can replace the item with one that is comparable.

4. If your art has damage, you’ll want to restore it to its original condition.

The right insurance company will provide the coverage you need and the resources to help protect your investment against loss. For example, your insurance broker can help you get risk assessments for your cellar or offsite storage facility. They can use infrared to detect harmful environmental conditions, and help you prepare for and respond to natural and man-made disasters to keep your collection safe.

Many homeowner’s policies exclude coverage for breakage of fragile items, like crystal, china and porcelain. The right insurance policy will automatically cover you for breakage. It will also cover your newly acquired artwork for up to 90 days, for up to 25% of the total itemized fine and decorative art coverage. That way, you don’t have to worry about getting insurance for each item on the day you purchase it.

The right insurance company will provide the coverage you need and the resources to help protect your investment against loss. For example, your insurance broker can help you get risk assessments for your cellar or offsite storage facility. They can use infrared to detect harmful environmental conditions, and help you prepare for and respond to natural and man-made disasters to keep your collection safe.

5. You may need to have your artwork transported.

If you do need to relocate your artwork, make sure your items are covered at all times. The majority of fine and decorative art losses occur while items are in transit. Your insurance company should be able to provide referrals to vetted art transporters you can trust.

Protect your fine and decorative art

With the market for fine and decorative art continuing to grow, it’s more important than ever to protect your valuables and ensure that they can be replaced if they are stolen, broken, or damaged. Our fine art insurance coverage provides the highest quality protection, unparalleled claim service, and peace of mind.

Sources:

- The Art Basel and UBS Global Art Market Report 2020

- “Behind Joan Mitchell’s Market Revival,” MutualArt, August 28, 2018

“Top 10 Female Artists of 2018,” BLOUIN ARTINFO, December 17, 2018

“Records tumble for top female artists and the time-honoured fruits of attractively low estimates,” The Telegraph, May 29, 2018

Content provided by Chubb.